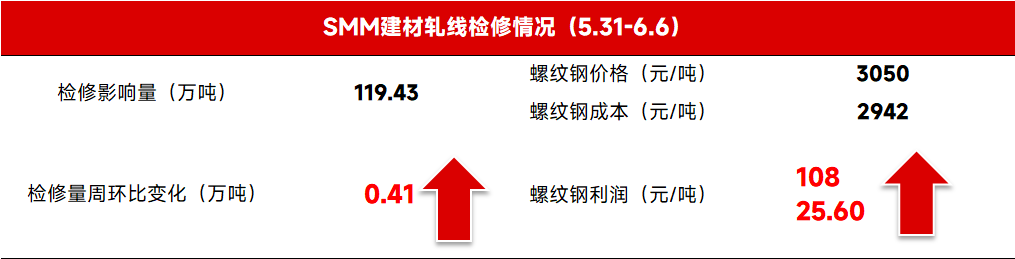

According to the SMM survey, the impact from maintenance on building materials increased slightly this week (5.31-6.6). Most steel mills extended maintenance from last week, while some added new rolling line maintenance plans. The impact from maintenance on building materials reached 1.1984 million mt, up 4,100 mt WoW.

Source: SMM

Last week, rebar futures broke through the 3,000-yuan level and continued to fluctuate downward with no clear rebound signs, dampening market confidence. Spot prices kept weakening, while coke and ore prices also declined. According to SMM calculations, blast furnace steel mills in east China still maintained profits of around 100 yuan, sustaining strong production enthusiasm. However, other regions, particularly north-west China, saw relatively poorer profitability, leading to weaker production motivation. The SMM survey showed this week's increase concentrated in north-west China, where some mills halted two bar rolling lines and one wire rod rolling line for maintenance, resulting in a slight rise in building material maintenance volume.

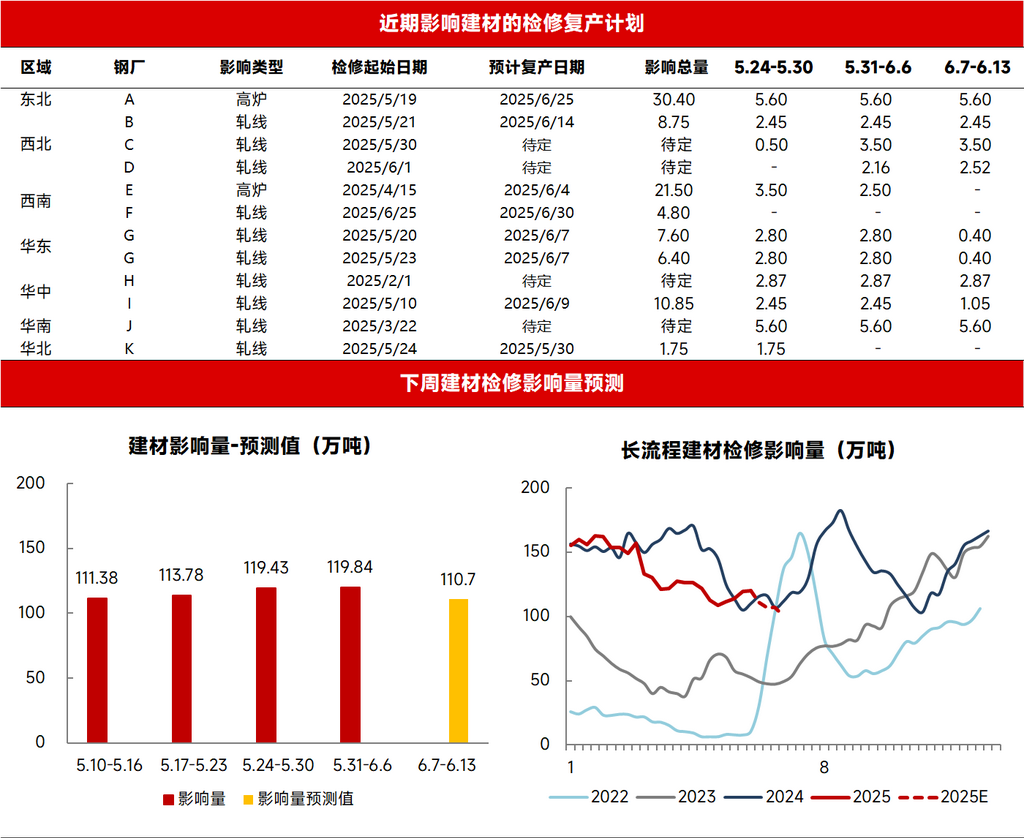

Looking ahead, increased rainy and high-temperature weather, coupled with approaching national college entrance exams, will further hinder construction progress in downstream industries. The traditional off-season for building material demand has arrived, offering weak short-term support for spot prices. Cost side, expectations persist for a third coke price drop, while ore prices may remain in the doldrums. Blast furnace steel mill gross margins are expected to have downside room, though the decline will likely be limited, with most mills maintaining previous production schedules. Based on current SMM surveys, mills in southwest and central China gradually resumed production, reducing total building material maintenance volume. However, considering long-term phased shutdowns of rolling lines in east China and Shandong mills adjusting annual production plans in response to crude steel output control policies, rolling lines may face halts or rotational material shortages. Next week's impact from maintenance on building materials is expected to see limited decline.

Source: SMM

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)